{kind=link}

There’s no question about it – keeping the Government Employees’ Retirement System from imminent bankruptcy was essential. In fact, the warning signs have been there for years – declining assets, negative cash flows, dire actuarial projections. But was the bond boondoggle contrived by the Bryan administration the only way to “Save GERS”? Absolutely not.

In order to understand the mechanics of this somewhat complex financial scenario you need to know several things about the retirement system, about rum taxes, and about excise taxes. The solution to the GERS problem – without getting into major structural reform in GERS itself – could have been achieved by a combination of revenue sources and good government discipline. And it would have avoided the very costly bond refinancing just completed by the Bryan administration.

The financial problem in GERS is, quite simply, that more money is being paid out than is coming in and the bank account is running precariously low. At the current rate of net expenditure GERS would have run out of cash reserves in 2024 at which point drastic measures would have had to be taken, including a possible reduction in retiree pensions.

The rum tax revenue (known as the “Internal Revenue Matching Fund” or IRMF) is an annual payment made by the U.S. Treasury to the Government of the Virgin Islands based on the number of gallons of rum produced in the USVI and sold in the U.S. We receive $13.25 per gallon of rum, and in the most recent year, with around 22 million gallons of rum sold, that amounted to $298 million in IRMF receipts.

Because of agreements signed by Gov. John de Jongh Jr. with Diageo and Cruzan (the two main rum producers in the USVI) roughly half of the IRMF is paid to the two rum companies. Whether or not this is a “good deal” for the USVI is debatable, but it is the deal and we live with it. So that leaves the V.I. government with around $150 million per year in IRMF revenue.

Over the years the V.I. government issued a number of bonds backed by that revenue stream. Bonds were issued in 2009, 2010, 2012 and 2013. The total “debt service” (principal plus interest payment) on those bonds was $85 million in 2021, and it would have declined to close to zero over the next 10 years as the bonds were paid off.

So the first option was to take the “residual” IRMF revenue – whatever was left over after paying principal and interest on the existing bonds – and allocate that revenue to GERS. However that, alone, would not keep GERS afloat over the next few years. It would have been adequate as the bonds were paid off and the residual increased, but there would still have been a shortfall for the next 3-5 years.

A second revenue stream available for consideration are the excise tax collections by the V.I. government. Several years ago the excise tax was halted following a legal challenge in federal court. That suspension was lifted last year after some minor policy changes relating to excise tax collections. The newly reinstated excise tax is estimated to amount to around $40 million per year, based on the last full year in which it was collected.

If we allocated 100 percent of the “new” excise tax collections to GERS, combined with a portion of the IRMF residuals, then GERS would remain solvent. No need for a bond boondoggle. No need to place a hefty debt burden on the shoulders of the next generation of Virgin Islanders.

But this approach was not politically expedient. Nobody could proclaim “VICTORY!” and say that they “solved the GERS problem.” It would have been a simple matter of budgeting and restraint on the part of this and future V.I. legislatures and governors.

Was the “GERS crisis” contrived in order to lay the groundwork for a major bond deal, with all of the political implications surrounding that in an election year? I don’t know. It is curious that a problem that has been brewing for many years was suddenly “solved” on the eve of a government election.

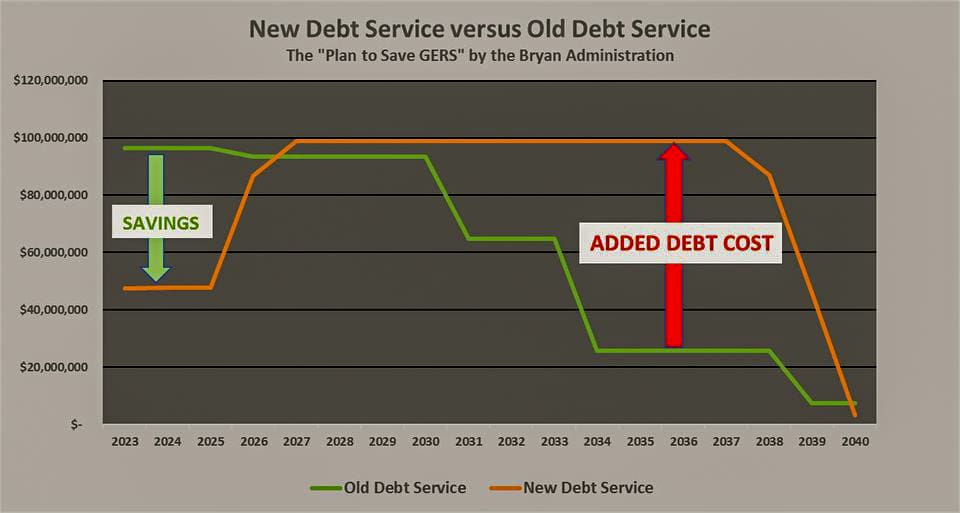

And to be clear, what is wrong with the “solution” created by the Bryan administration (with the unanimous support of the 34th Legislature)? The chart above tells part of the story – we’ve saddled the next generation of Virgin Islanders with a heavy burden of debt, unnecessarily. We’ve increased our total debt service by $360 million.

The other part of the story was the “giveaways” to the participants in the bond boondoggle. The governor’s advisors, lawyers, “strategic consultants” and other bond professionals received $15 million in fees. And the buyers of the new bonds will, over the lifetime of the bonds, receive a half a billion dollars in interest payments – $501,871,000 in interest. And none of that was necessary.

The alternative plan – without the Bryan Bond Boondoggle – would have allocated 100 percent of the renewed excise tax collections to GERS. It would have allocated 80 percent of the IRMF residuals to GERS, leaving an annual contribution (over $20 million per year on average) to the GVI General Fund. And GERS would have ended up with a healthy $1 billion in net assets.

So the obvious question is: Why didn’t they do this? And the obvious answer: POLITICS.

Sources: PFA bond prospectuses 2009, 2010, 2012, 2013, 2022; GERS actuarial report 2021; PFA annual reports; Cruzan and Diageo agreements

— David Silverman, Coral Bay, St John